HELOC Rates: A Comprehensive Guide to Understanding and Securing the Best Deal

A Home Equity Line of Credit (HELOC) can be a powerful financial tool, offering flexible access to funds secured by your home’s equity. However, navigating the world of HELOC rates can be confusing. This comprehensive guide will demystify HELOC rates, explaining the factors that influence them, how to compare offers, and strategies for securing the best possible rate.

Understanding HELOC Rates: The Basics

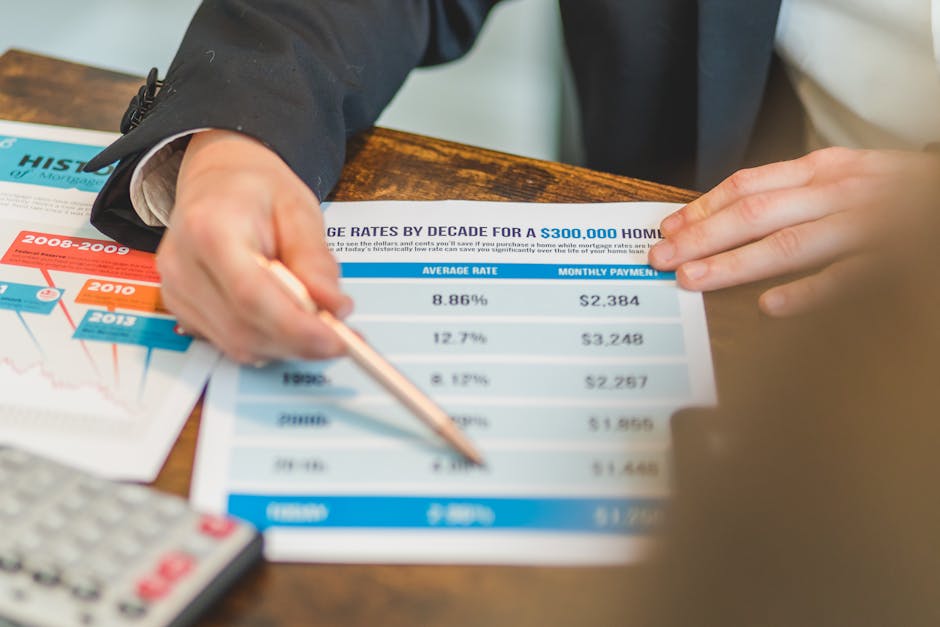

Unlike fixed-rate loans, HELOCs typically feature variable interest rates. This means your interest rate—and consequently, your monthly payments—can fluctuate over the life of the loan. These rates are usually tied to an index, such as the prime rate or the London Interbank Offered Rate (LIBOR), plus a margin set by your lender. The index reflects broader economic conditions, while the margin represents the lender’s profit.

Key Terminology

- Index Rate: The benchmark rate your HELOC’s interest rate is based on. This rate fluctuates with market conditions.

- Margin: The percentage added to the index rate to determine your overall interest rate. This is a fixed amount set by your lender.

- Annual Percentage Rate (APR): The annual cost of borrowing, including the interest rate and any fees. The APR provides a more complete picture of the loan’s cost than the interest rate alone.

- Draw Period: The time frame during which you can borrow money from your HELOC.

- Repayment Period: The period after the draw period during which you must repay the borrowed amount.

Factors Influencing HELOC Rates

Several factors significantly impact the HELOC rate you’ll receive. Understanding these factors will help you negotiate a better deal and improve your chances of securing a lower rate.

Credit Score: Your Foundation for Favorable Rates

Your credit score is arguably the most crucial factor. Lenders consider your creditworthiness when setting your margin. A higher credit score indicates lower risk to the lender, leading to a lower margin and a more favorable interest rate. Aim for a score above 700 for the best possible rates.

Loan-to-Value Ratio (LTV): How Much Equity You Have

Your LTV is the ratio of your mortgage loan amount to your home’s current market value. A lower LTV signifies greater equity in your home, reducing the risk for lenders and often resulting in lower HELOC rates. The more equity you have, the better your chances of getting a lower rate.

Debt-to-Income Ratio (DTI): Managing Your Financial Obligations

Your DTI reflects your monthly debt payments relative to your gross monthly income. A lower DTI indicates better financial health and responsibility, which lenders view favorably, potentially leading to a better HELOC rate. Managing your debts effectively will strengthen your application.

The Current Economic Climate: Market Forces at Play

HELOC rates are sensitive to broader economic conditions. When interest rates rise generally, HELOC rates tend to follow suit. Conversely, during periods of low interest rates, you may find more competitive HELOC offers. Stay informed about current economic trends.

The Lender: Comparing Offers is Key

Different lenders have different lending criteria and rate structures. Shopping around and comparing offers from multiple lenders is essential to secure the most competitive HELOC rate. Don’t settle for the first offer you receive.

Tips for Securing the Best HELOC Rates

Obtaining the best HELOC rate requires proactive planning and strategic steps. Here are some tips to help you achieve your goal:

Improve Your Credit Score: A Long-Term Strategy

Work on improving your credit score before applying for a HELOC. This involves paying bills on time, keeping credit utilization low, and avoiding opening numerous new accounts in a short period.

Shop Around and Compare: Don’t Rush the Process

Compare offers from multiple lenders, considering not just the interest rate but also fees, terms, and other conditions. Use online comparison tools and seek pre-approval to get a better understanding of what’s available.

Negotiate with Lenders: Leverage Your Strengths

Don’t hesitate to negotiate with lenders, particularly if you have a strong credit score and a low LTV. Highlight your financial strength to potentially secure a lower margin or other favorable terms.

Understand the Fine Print: Avoid Hidden Costs

Carefully review all loan documents, paying attention to fees such as origination fees, annual fees, and closing costs. These fees can significantly impact the overall cost of the HELOC.

The Drawbacks of HELOCs

While HELOCs offer flexibility, it’s crucial to understand potential drawbacks:

- Variable Interest Rates: Fluctuations in the index rate can lead to unpredictable monthly payments.

- Risk of Foreclosure: Failure to repay the loan could result in foreclosure on your home.

- Fees: Various fees associated with HELOCs can add to the overall cost.

Conclusion

Securing a favorable HELOC rate requires a comprehensive understanding of the factors involved and proactive steps to improve your financial standing. By following the strategies outlined in this guide, you can significantly increase your chances of obtaining a competitive rate and utilizing the benefits of a HELOC responsibly.